Celebrating our Client's Successes

Success Stories

Simplifying the liquid fuel payment guarantee process.

-

Available Cash Payment Guaranteed.

-

Insurance Guarantees.

-

Fuel Finance / Facility.

-

Empowering and assisting the establishment of new entrants.

-

Improving the processes for existing / established industry participants.

Simplifying the liquid fuel payment guarantee process.

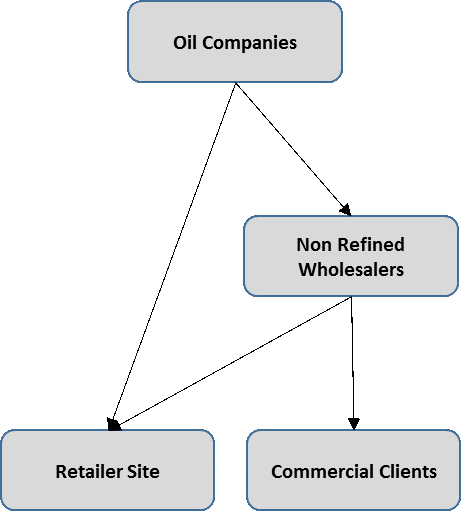

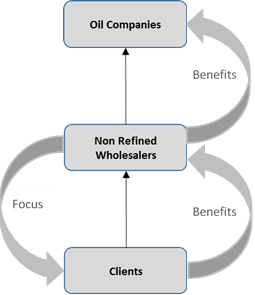

Through G-PAY™ we have been involved in the Liquid Fuels Industry since 2011 and on a high level we understand the industry to be divided into several tiers/levels for distribution and sales. These start with the Oil Companies and Refineries (The Majors) who provide and sell to lower tiers/levels. These being direct to Oil Company owned/branded Retailer sites, Non-Oil Company owned (White) sites and also to Non-Refining Wholesalers (NRW’s) who make up a large volume of their sales. The Majors also in some instances sell product directly to some of the larger Commercial Clients.

NRW’s in return service their own client base which could consist of Retail Sites but mainly Commercial Clients who purchase in Bulk.

Product is mainly held in storage by The Majors although some NRW’s may have their own smaller storage facilities. These facilities are often used for the sales of smaller quantities to the NRW customers. The product is generally sold on a Client Own Collection (COC) or a Delivered by The Major or NRW basis. COC refers to the process whereby a client would collect product from The Major or NRW while the delivered portion is done by The Major or NRW as may be applicable. COC and Delivered is also a term used in the pricing structures provided by The Major or NRM as these models attract different pricing schedules.

Industry Challenges.

The industry is experiencing challenges on several levels, The Majors mainly provide product and do not really experience the same challenges as would be the case for NRW’s / Retailer / Commercial Clients.

Distinctions also need to be made between the established NRW’s, new entrants in the NRW level and the challenges that reflect the Retailers and Commercial Clients situations.

The NRW (Existing) – NRW’s and/or their clients currently have bank guarantees and other forms of security pledged to The Major to secure a supply of product. Majors will generally only provide product to its customers within the boundaries of these guarantees and securities. When these are depleted the Retailer and or NRW can only continue purchasing on a cash upfront basis and we understand cash flow to be the largest challenge for these entities.

The reality is that the guarantees and security provided are not regularly maintained and or adjusted by the financial institution during the course of the relationship as the fluctuation in the fuel price is affected which has a direct influence on the client and NRW cash flow position. An increase in the fuel price means that the Client / NRW measured against a fixed guarantee which means they can purchase less for their allocated value, while a decrease in the fuel price will provide the opposite. History has however shown the fuel price has mostly increased, occasionally decreases occur but never below the general growth norms. This tendency affects new Clients and NRW entrants to the market even more than it does the more established Clients and NRW’s.

The general rule with The Majors is also that no product is released until paid for in full whether it be under the guarantee / security option or as a cash customer. This rule in general provides the largest single challenge to the industry especially out of guarantee / security transactions but more specifically for the cash customers.

In the instruments developed through the G-PAY™ solution offerings there is also opportunity to establish a “clean invoicing” model as the G-PAY™ technology offers the ability to lock funds which can be guaranteed from client, to NRW all the way through to the Majors for settlement of the actual collected or delivered quantities.

These NRW and Client challenges offer the opportunity for the implementation and deployment of the G-PAY™ instruments and solutions.

The NRW (New Entrant) – For these entities the challenge above is even more overwhelming. These entities normally do not have a proven track record, financial track record to obtain guarantees from financial institutions, and do not have the financial backing or the ability to pre purchase product. The Majors policy “Payment Before Collection” of the product also does not favor their position.

Clients are very reluctant to pay the NRW before they have received their product. This leaves the new entrant NRW in a position where his/her business is not going anywhere. The Department of Energy has issued an unknown number of NRW licenses in the past 5 years but only a handful have managed to do “some” business but they are not managing to retain these clients as they are not able to offer competitive solutions to customers.

These New NRW challenges offer the opportunity for the implementation and deployment of the G-PAY™ instruments and solutions.

The Clients – Most clients are accustomed to having to pay upfront for product at the moment but the demand for extended payment terms is increasing. The Majors and the NRW’s are however not always in a position to provide terms to these clients.

These client challenges offer the opportunity for the implementation and deployment of the G-PAY™ instruments and solutions.

Industry Solutions.

The solutions through G-PAY™ are configurable and may be applied differently on a case by case basis depending on the level of deployment, the client profile, risk and control to be asserted on the control over the funding and the unique G-PAY™ ability to verify the availability of funds in the account on creation of the order, the ability to then reserve the funds against the Selling entity, the ability to lock the funds upon acceptance of the order by the selling entity, and thereafter to guarantee the payment to the selling entity. In this solution G-PAY™ further offers the ability to on/after delivery reconcile the order payment to the actual delivered/collected quantities, eliminating the issue of over/under deliveries/collections which enables clean invoicing based on only the confirmed order quantity value being processed from the buyer to the seller account. This functionality is supported by the G-PAY™ host integration with the banks.

Referring to the tiers mentioned earlier (The Majors, The NRW and The Clients) G-PAY™ further offers the ability to settle all three ties in the same transaction from funds held in the lowest tier, the client. This includes the pricing structures that have been defined between the parties for the various levels.

The above in its simplest format defines the capabilities, functionality and the G-PAY™ ability to offer a new and unique way of guaranteeing payments and providing an electronic/digital guarantee for processing through G-PAY™.

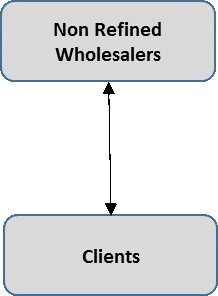

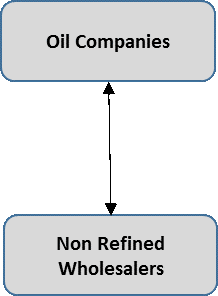

Two Tier Models – Where funds reside at the lower lever, G-PAY™ will first verify the availability of funds in the buyer account, reserve and lock the funds allowing the delivery or collection to take place after which the actual delivered/collected quantities will be confirmed. Only after confirmation of the delivered quantities will the funds be processed from the buyer to the seller. This model therefore caters for transactions between clients and NRW’s or between NRW’s and The Majors.

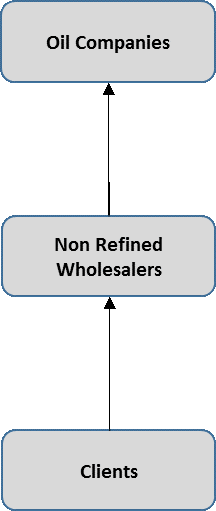

Three Tier Models – In a three-tier model configuration, the G-PAY™ system, assuming that the funds reside with the client, will settle both the top tiers on completion of the delivery or collection of the order. By means of an example pricing structure, with the client price with the NRW being R10.00, and the NRW price with the Oil Company being R8.00, the G-PAY™ system will automatically calculate and process as follows:

- The system will process R10.00 from the Client to the NRW. Immediately process R8.00 to the Oil Company leaving R2.00 in the NRW account. Where fees have been set, the system will also process these fees from the client to the appropriate party.

- Variations on the above models – Where authorization for every transaction is required, we can implement the standard G-PAY™ software which can be configured to workflow a transaction to the appropriate party for authorization before processing on either of the levels.

- Although the standard G-PAY™ Solution and functionality, based on available cash in the clients account, already suggests a solution to the Liquid Fuels industry, we have also developed Financing Solutions, Insurance Guarantees and other instruments to offer to the industry.

In Summary.

Traditionally the focus from Financial Institutions and The Majors have been on the capability and the credit and risk profile of the NRW and its ability to provide Security, Guarantees and other similar instruments to achieve an allocation or product from the Majors. The G-PAY™ Solutions have created the ability to shift such focus from the NRW to the NRW Clients.

With the focus now being on the NRW Clients and not the NRW being evaluated for such facility, the risk is not only mitigated for the Financial Institutions, but it also enables New NRW entrants to start a business and it offers existing NRW’s the capability to expand their business (product volumes). In fact, the NRW business size is no longer dictated or restricted by the Security, Guarantees and other similar instruments provided by the NRW, but rather the NRW’s ability to sell. The benefits of such model is passed from the Client to the NRW and rolled up to the Majors.

Please contact us for more information on the G-PAY™ instruments and models available to the Liquid Fuels sector.

SME’s more fundable.

-

Keeping track of the cookies.

-

Lock-Box unlocks SME growth potential.

Modernising futures contracts for the fuel industry

-

Facilitating the hedging of diesel futures contracts.

-

Physical contract execution.

-

Contract settlement.

Solving the payment challenges of allocating funds to a 3rd party in Agriculture

-

Facilitating variable funding models. (reallocation of bank facility).

-

Enabling extended payment terms.

-

Automated sweeping / settlements for extended payment terms.

-

Emerging & Established farmer empowerment configuration models.

Protecting investor funds

-

Enabling cash management disciplines.

-

Closed loop procure to pay models.

-

Closed loop beneficiary payment models.

-

Cashflow Waterfall solutions.

-

Transactional mapping and reporting.

e-Escrow

-

Enabling financial institutions to digitise traditional Escrow models.

-

Enabling financial institutions to automate traditional Escrow processes.

-

Enabling closed loop or open loop Escrow solutions.

-

Enabling procure to pay solutions in e-Escrow.

-

Comprehensive e-Escrow functionality.